The global lever-lid tinplate container market is entering a strong growth cycle, supported by booming e-commerce logistics, rising consumer expectations for durable packaging, and industry investments in modern tinplate production lines. These containers, recognized for their metal-lever sealing design, continue to gain traction across food, paint, ink, and chemical applications due to their excellent strength, tamper resistance, and recyclability.

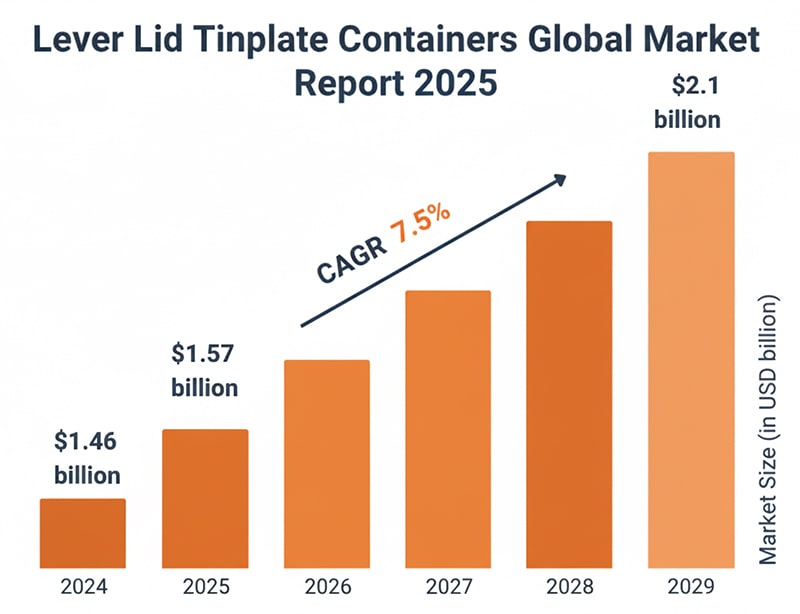

According to industry analysis, the market reached $1.46 billion in 2024 and is projected to grow to $1.57 billion in 2025, marking a 7.5% CAGR. Looking ahead, revenue is expected to rise to $2.1 billion by 2029, supported by surging production automation and rising demand for long-shelf-life packaging solutions.

The lever-lid tinplate packaging category is on track to hit $2.1 billion by 2034, reflecting a continued 7.5% CAGR from 2025 onward. Growth momentum is linked to:

Expansion of global e-commerce and retail networks

Higher performance requirements for shipping-safe packaging

Regulatory support for metal recycling and circular economy initiatives

Design upgrades such as lacquer-coated and digitally printed tinplates

Asia-Pacific leads the global market, with strong manufacturing activity in China, India, and Southeast Asia. Europe and North America follow, driven by premium food and paint segments.

Lever-lid tinplate containers are typically steel cans coated with tin or aluminum, equipped with a mechanical lever closure. They are favored in markets requiring secure sealing — paint and coatings, edible products, adhesive chemicals, solids and powders, and craft storage.

They are commonly offered in capacities ranging from 125 ml to 15,000 ml.

Growing online retail logistics are pushing demand for impact-resistant, leak-proof packaging. Lever-lid cans protect sensitive contents (inks, chemicals, specialty food items) during transportation.

Recent government data indicates the trend clearly: U.S. e-commerce sales rose 8.5% YoY in Q1 2024, outpacing overall retail growth (2.8%).

Geopolitical trade adjustments — particularly between the U.S. and Asian export nations — are influencing tinplate and steel input prices. Higher tariffs on imported tinplate from China and South Korea are expected to affect North American paint, chemical, and food packaging costs.

Companies are actively expanding production infrastructure to keep supply ahead of demand. In June 2024, for example, Invopak opened a €5M Manchester facility, bringing tinplate can manufacturing in-house to enhance agility amid post-Brexit logistics shifts.

Meanwhile, Tata Steel’s 2024 merger with Tinplate Company of India Ltd. further strengthens domestic tinplate supply in Asia.

Metal (steel & alloys)

Tin

Steel (carbon, stainless)

Aluminum (coated & uncoated)

125–250 | 250–500 | 500–750 | 750–2500 | 2500–5000 | 5000–15000

Food | Chemicals | Paints & Coatings | Inks | Other industrial uses

| Year | Market Value |

|---|---|

| 2024 | $1.46B |

| 2025 | $1.57B |

| 2029 | $2.1B |

| 2034 | $2.1B (forecast target milestone) |

| CAGR (2025-2034) | 7.5% |

Amcor plc

Crown Holdings Inc.

Sonoco Products Co.

Silgan Holdings

Toyo Seikan Group

Ardagh Metal Packaging

Mauser Packaging Solutions

Visy Industries

Dongguan Suno Packing

Central Tin Containers Ltd.

(and more)

As a tinplate packaging manufacturer’s perspective: The tightening of global recycling laws and premiumization in consumer goods are reshaping metal packaging standards. Customers increasingly request:

Direct-printing tinplate finishes

BPA-free internal coatings

High-pressure sealing rings

Automated handle & rim stitching

Factories investing in robotic seam welding, energy-efficient annealing, and inline leak-testing systems will lead the next competitive cycle. Additionally, brands in baby formula, luxury snacks, and artisanal paints are moving toward custom-shape tins, signaling a shift from commodity cans to value-enhanced metal packaging.

Obtenha as últimas informações e ofertas especiais

Rede IPv6 suportada

Rede IPv6 suportada Português

Português English

English Français

Français Deutsch

Deutsch Español

Español